I start every year by reviewing the long-term technical positions and behaviors of the “Large 4” — 10-year yields, S&P 500 ($SPX), Commodities, and the US Greenback. I consider that rates of interest, notably in a credit-dependent/leveraged system, usually drive financial and market cycles. And, since by career I’m a charges/credit score portfolio supervisor, strategist, and dealer, I all the time start there.

Granted, a macro view would not usually inform short-term buying and selling, however something that helps me perceive the ebb and move and interconnectedness of markets is useful. Extra importantly, recognizing markets aligned for vital macro change may be invaluable, notably when it comes to threat administration.

Since most good technical evaluation is fractal, the identical methods used to explain the macro ebb and move can usually translate to shorter time frames. For the primary twenty years of my buying and selling profession, I saved a guide grid of the Large 4 plus a couple of different markets (gold, oil, 2-year Treasury, and so forth) that I up to date hourly with value and the change from the prior hour. Doing so taught me a fantastic deal about market interactions and interrelationships.

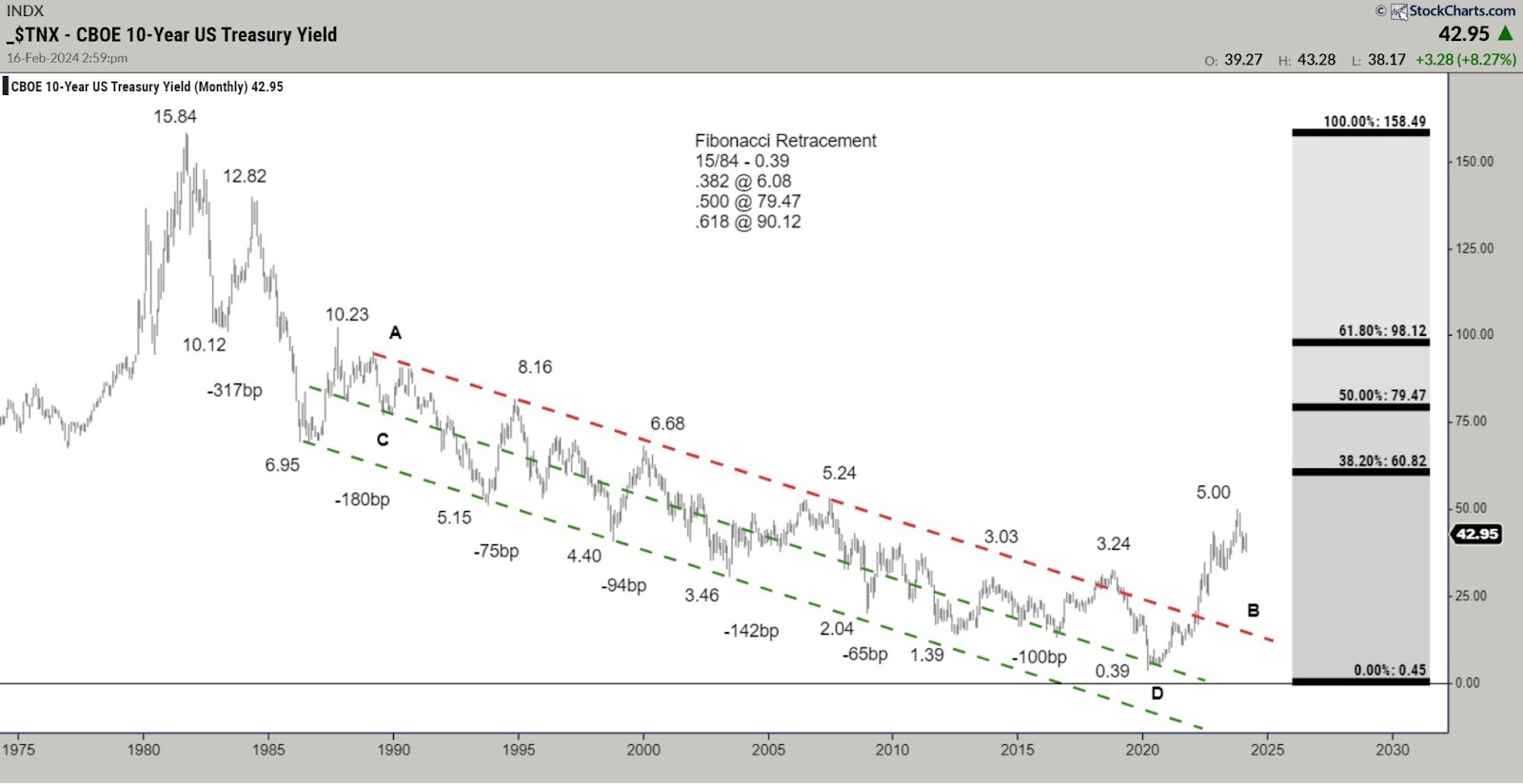

Month-to-month 10-12 months Word Yield

CHART 1. MONTHLY CHART OF 10-YEAR TREASURY YIELDS Over the past 4 a long time, bond yields had constantly and reliably made decrease highs and decrease lows. Your complete bull market was outlined by a broad declining channel (A–B, C–D). The A–B downtrend line represented the “stride of demand,” or the zone the place patrons constantly emerged, and the C–D line represented the “overbought line,” or the zone the place provide or sellers constantly emerged.

Take Word. Falling bond yields are synonymous with increased bond costs. In different phrases, a downtrend in yield = a bull market in bonds.

From 2012 ahead, there have been rising indicators that the lengthy downtrend was growing old. 4 issues stood out.

- The repeated failure to push to the oversold line (C–D).

- The flattening out of the decline, the place every push to a brand new yield low solely lined round 100 bps.

- The 2018 spike to three.24% that weakened the first A-B downtrend.

- The bond push to the world across the middle of the channel, and failure to push past the midline, a lot much less into the overbought line (C–D), in March 2020. This transformation of habits strongly advised that demand was tiring. A number of seen modifications in habits strongly advised that the 40-year downtrend was in peril of terminating.

The clear break and acceleration above the A–B downtrend have moved the lengthy development from bullish to impartial. Whereas it is possible that the transfer above the November 2018 pivot at 3.24%, coupled with the prior habits modifications, mark the start of a long-term bear market, a better low (maybe forming in 2024) is required to finish/affirm that change.

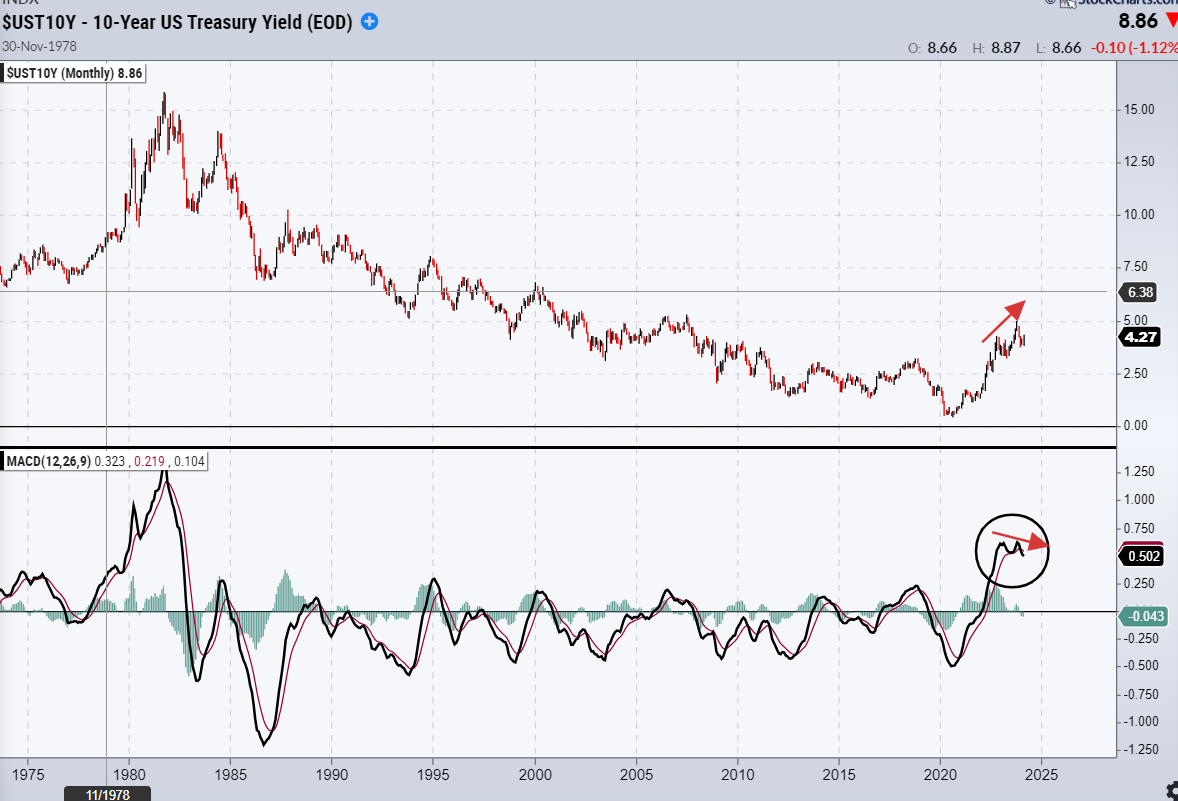

Word the extra modifications in habits. The 459 bps transfer from 0.39% to 4.98% represents the only largest bearish transfer for the reason that inception of the bull market in September 1981, and the MACD oscillator degree far exceeded the degrees that marked yield highs all through your complete bull market.

10-12 months Yield Month-to-month With MACD

After producing probably the most overbought studying for the reason that Nineteen Eighties, the oscillator is making an attempt to roll over and is displaying a small unfavourable divergence (suggesting decrease yields and better value). Whereas not a definitive roll, it suggests that there’s some potential for a significant flip.

CHART 2. MONTHLY CHART OF 10-YEAR NOTE YIELD.

10-12 months Yield Weekly

With this subsequent chart, I’ll work with the weekly perspective, 5 and ten-year charts, and yield curves.

CHART 3. WEEKLY CHART OF 10-YEAR YIELD.

The next are a number of key elementary factors round charges:

- The defining macro attribute of the 40-year bull market has been the continuous fall within the inflation fee. If that’s altering (I consider it has), the secular bond development is probably going additionally to vary.

- If the development in inflation modifications, the unfavourable correlation between bonds and fairness that drives 60/40 allocation and threat parity investing is prone to flip and turn into constructive. In different phrases, bonds and fairness would, outdoors of intervals of panic or financial misery, rise and fall collectively, destroying the diversification profit. This has been the historic norm, and I anticipate the market to maneuver in that route steadily.

- The caveat: Quantitative easing eliminated the worth proposition from bonds; when equities started to say no in 2022, bonds could not present a protected haven. They have been already far too costly, notably within the context of a Federal Reserve aggressively tightening financial coverage. That’s now not the case. Bonds, whereas nonetheless costly, can once more present a tactical hedge ought to threat belongings or the economic system weaken dramatically.

- At first look, this appears at odds with the change in correlation mentioned above, however it’s a distinction between the secular tide versus the intermediate wave.

- Most substantive bond rallies outcome from a disaster that creates a flight-to-quality. In an excessively financialized and levered economic system, rising charges usually break the weakest hyperlink within the financial chain, creating a brand new disaster and a subsequent flight-to-quality rally. Whereas there’s little proof of a systemic disaster, the lagged impact of the fast enhance in charges in an excessively financialized system have to be high of thoughts.

The Backside Line

Whereas there’s nonetheless extra work to be finished to verify the development change, I consider the bond development is lastly altering, because the world strikes from the deflationary backdrop of the final a number of a long time to an inflationary backdrop. I will likely be a a lot better vendor of rallies and bearish technical setups within the weekly/intermediate perspective.

Disclaimer: Shared content material and posted charts are meant for use for informational and academic functions solely. The CMT Affiliation doesn’t provide, and this info shall not be understood or construed as, monetary recommendation or funding suggestions. The data offered shouldn’t be an alternative to recommendation from an funding skilled. The CMT Affiliation doesn’t settle for legal responsibility for any monetary loss or injury our viewers might incur.

Good Buying and selling.

Stewart Taylor, CMT

Chartered Market Technician

Stewart Taylor retired from Eaton Vance Administration in January 2020 after a 40-year profession in US fastened revenue with an emphasis on technical evaluation and relative worth investing. He joined Eaton Vance because the Senior Dealer for the Funding Grade Fastened Revenue staff in 2005. Throughout his tenure, he was a portfolio supervisor for institutional separate accounts and mutual funds, managed the staff’s inflation belongings, and was the staff’s strategist for period, relative worth, and financial positioning. From 1992 to 2005, he offered personal investing and buying and selling session to institutional purchase aspect, broker-dealers, and hedge funds.

Be taught Extra