{kind=link}

2012 was the 12 months of the Seedpocalypse. Additionally known as the Collection A Crunch, a worry gripped Startupland : elevating a Collection A. Two years later, this indigestible extreme bolus of fundraising rounds hit the Collection B market & Collection Bs turned essentially the most difficult spherical to boost.

Each time there are “too many” of fundraises of 1 kind, the following spherical turns into the toughest to boost.

In 2024, the Collection A Crunch has returned. Software program corporations which have achieved the earlier period’s milestone, $1m or extra in ARR, face a difficult Collection A market. Why is that this occurring once more?

Simply as in 2012, a surge in seed investments met a comparatively steady Collection A market. The provision/demand imbalance creates a funding squeeze.

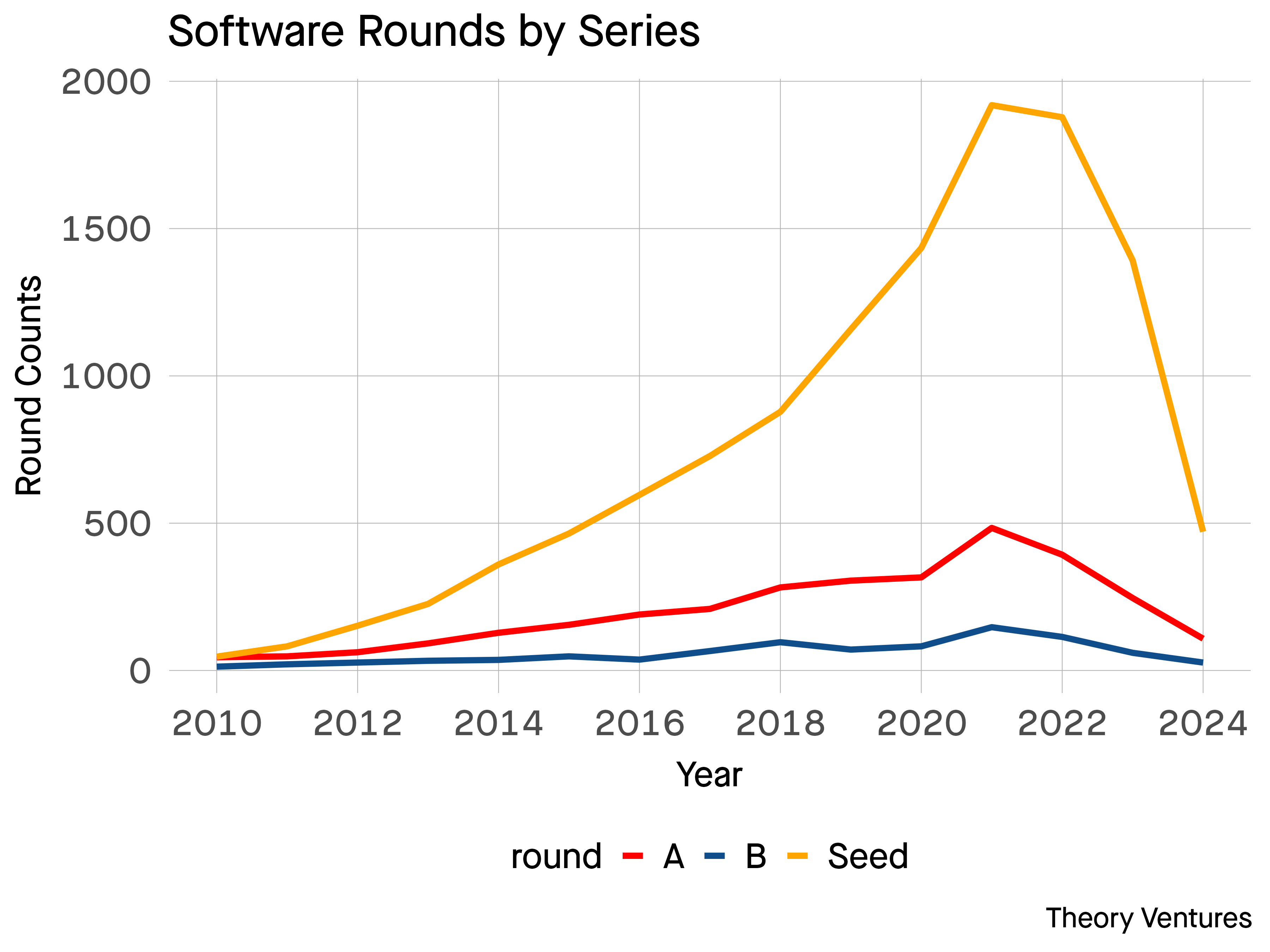

The orange crush of seed funding has outpaced the expansion in Collection A & Collection B rounds. Many new seed funds began & the speed of firm formation surged in the course of the early 2020s pushed by an ebullient capital markets.

Additionally, the definition of a Seed spherical has modified. The Seeds of the 2010 period are the pre-Seeds of right now, making the comparability impure.

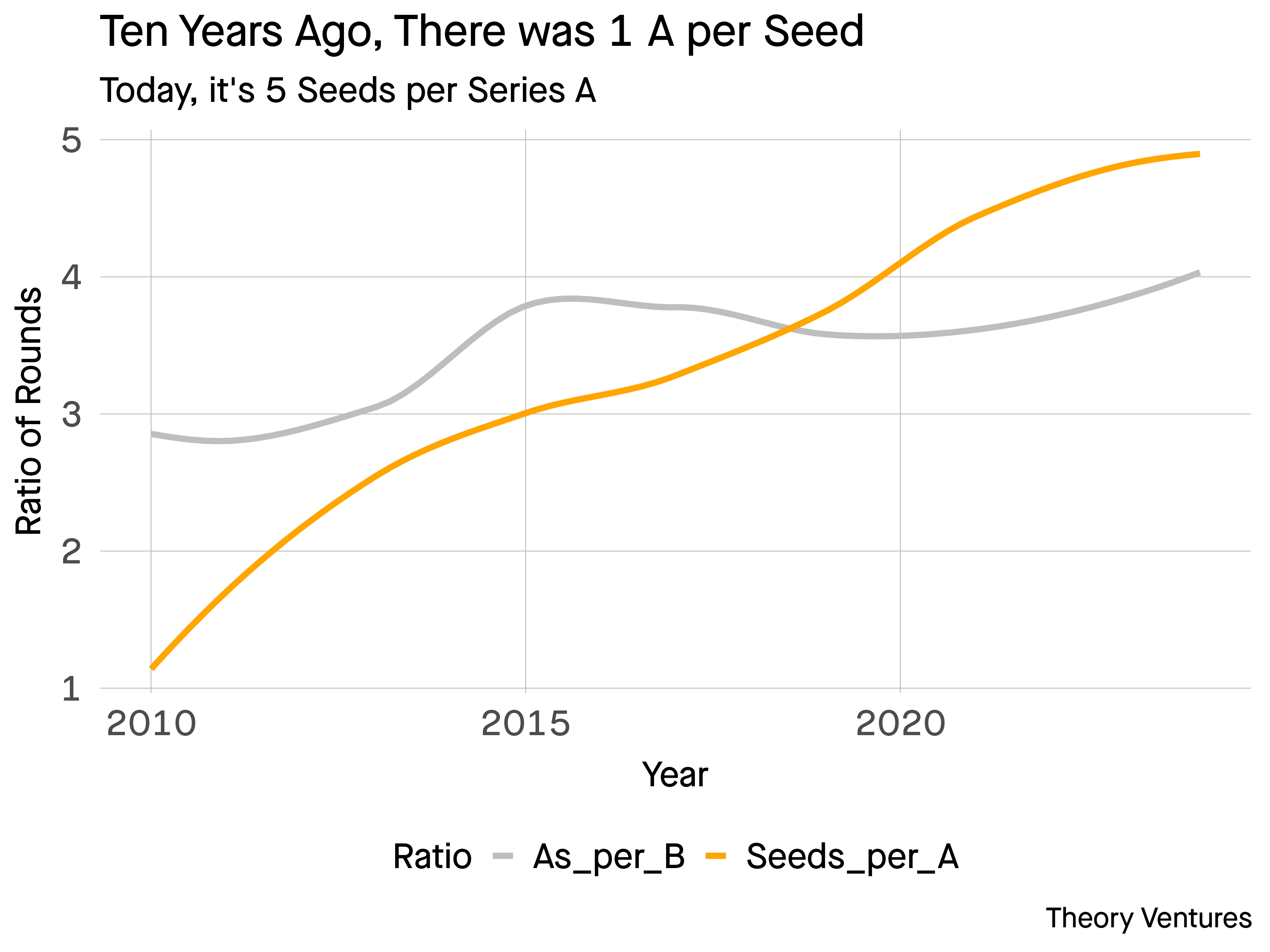

Regardless, Collection As haven’t grown to just about the extent of Seeds. Over the last 14 years, the ratio of Seeds to Collection As has grown from about 1.1 to 1, to five to 1. In the meantime, the ratio of Bs to As is comparatively fixed : between 3 & 4 to 1.

With extra seed provide & in an period the place ahead public software program multiples have reverted to the imply from their stratospheric ranges, Collection A rounds are more durable to boost. AI startups, the darlings of the present period, are a notable exception. On this class, the heady multiples of 2021 & 2022 nonetheless apply.

However for traditional SaaS corporations, the Collection A Crunch is actual. In 18 months, the Collection B will once more turn into the toughest spherical to boost.