{kind=link}

By Aimee Raleigh, Principal at Atlas Enterprise, as a part of the From The Trenches characteristic of LifeSciVC

From the skin, one may assume all biotech enterprise capital (VC) companies are extra related than completely different. Nonetheless, when you look underneath the hood the myriad traits distinctive to every agency turn into extra obvious, even for companies that will co-invest in the identical corporations once in a while. Whereas not by intent, the trade can appear opaque purely as a result of there are comparatively few buyers and little or no is publicized in regards to the internal workings of enterprise. Specializing in the U.S. VC panorama, there are ~90 biotech VC companies with belongings underneath administration (AUM) ≥ $1B (by way of Pitchbook) – on the finish of the day that’s not a really giant quantity, in all probability translating to the excessive lots of to low 1000’s of particular person biotech buyers (in comparison with, for instance, the tens of 1000’s of life sciences consultants within the U.S.). By way of this submit I hope to shed extra gentle on the trade, and particularly early-stage biotech VC since that’s my particular person bias. Beneath are some issues I believe useful for anybody new to the biotech VC world, together with potential investor candidates or firm founders.

There are completely different flavors of biotech VC. Biotech, life sciences, and healthcare VC are sometimes used interchangeably, however there’s a modestly sized “universe” of VC companies that will fall inside this umbrella.

-

- The primary axis on which to section companies is focus – sometimes cut up into therapeutics, medical units, healthcare companies, and IT. Some companies might be true generalists masking many, if not all, of those classes, and others might be fairly slender in focus. Atlas Enterprise is amongst a sizeable cohort of buyers that focus completely on therapeutics investing – given my bias the rest of this dialogue will take a therapeutics investing-focused lens.

- The second axis of differentiation is firm stage at which a VC sometimes invests. “Early stage” typically encompasses Seed- or Collection A-stage offers. Buyers targeted on early-stage corporations will possible proceed to fund corporations via later rounds (Collection B and past), however could not sometimes put money into new alternatives past the Collection A. Later-stage companies sometimes concentrate on offers which might be Collection B and past (together with what is taken into account “crossover” investing to bridge to an IPO), although relying on macro situations can even come into historically “early” Collection A offers. Stage-agnostic buyers will make investments throughout the spectrum. So why does understanding the standard stage at which a agency invests matter? Usually stage is intricately linked with valuation, maturity of the corporate and / or program(s), and time to worth inflection (and thus potential “exit” to the general public markets or to acquisition by a Pharma). Early-stage buyers are sometimes extra more likely to play some function in firm formation or firm constructing, given they could be among the first cash in and might help to play a key function in informing an organization’s technique. Later-stage buyers should still take an energetic function, however are sometimes investing when extra of the workforce and technique has been (not less than initially) constructed out and the thesis has been partially de-risked.

- One other axis is enterprise mannequin. Is the corporate platform- or asset-centric, or a mixture of each? In the end each profitable remedy that makes it to sufferers is a person asset, so sooner or later even platform corporations can shift to an asset focus. Some buyers are strict within the varieties of corporations they put money into (e.g., solely specializing in single-asset theses or requiring a platform to de-risk the potential that anyone asset fails). Understanding any investor preferences early-on is vital to understanding your match, both as a portfolio firm if you’re a founder or as a workforce member if you’re a potential candidate.

- Fund measurement, decision-making construction and any therapeutic space– or modality-centric funding preferences are additionally vital to know, although these will be tougher to glean throughout preliminary diligence of a agency.

- And eventually, location is to not be ignored, particularly within the context of the above. A stage-agnostic VC who could also be extra hands-off is probably going comfy with investments throughout a spread of geographies, whereas firm constructing companies could want to construct regionally.

Fast abstract: If you’re a possible candidate enthusiastic about a job in VC or an organization founder making an attempt to determine how greatest to pitch to VCs, I strongly suggest beginning with a refined listing of these companies most related to your background, curiosity, firm, thesis, and many others. Begin with an Excel of all of the biotech VCs you’ll be able to title, and filter by focus space, stage, enterprise mannequin, and site. A few of this data might be available on agency web sites, or else will be intuited by energetic portfolios. It’s not anticipated that you’d have the ability to work out every little thing, however a fast search ought to offer you a good suggestion whether or not you (or your organization) could be a very good match. And in a primary name with an investor, don’t be shy about asking for specifics! Every agency is exclusive in its construction and tradition, which interprets to variations in funding choices and portfolio development.

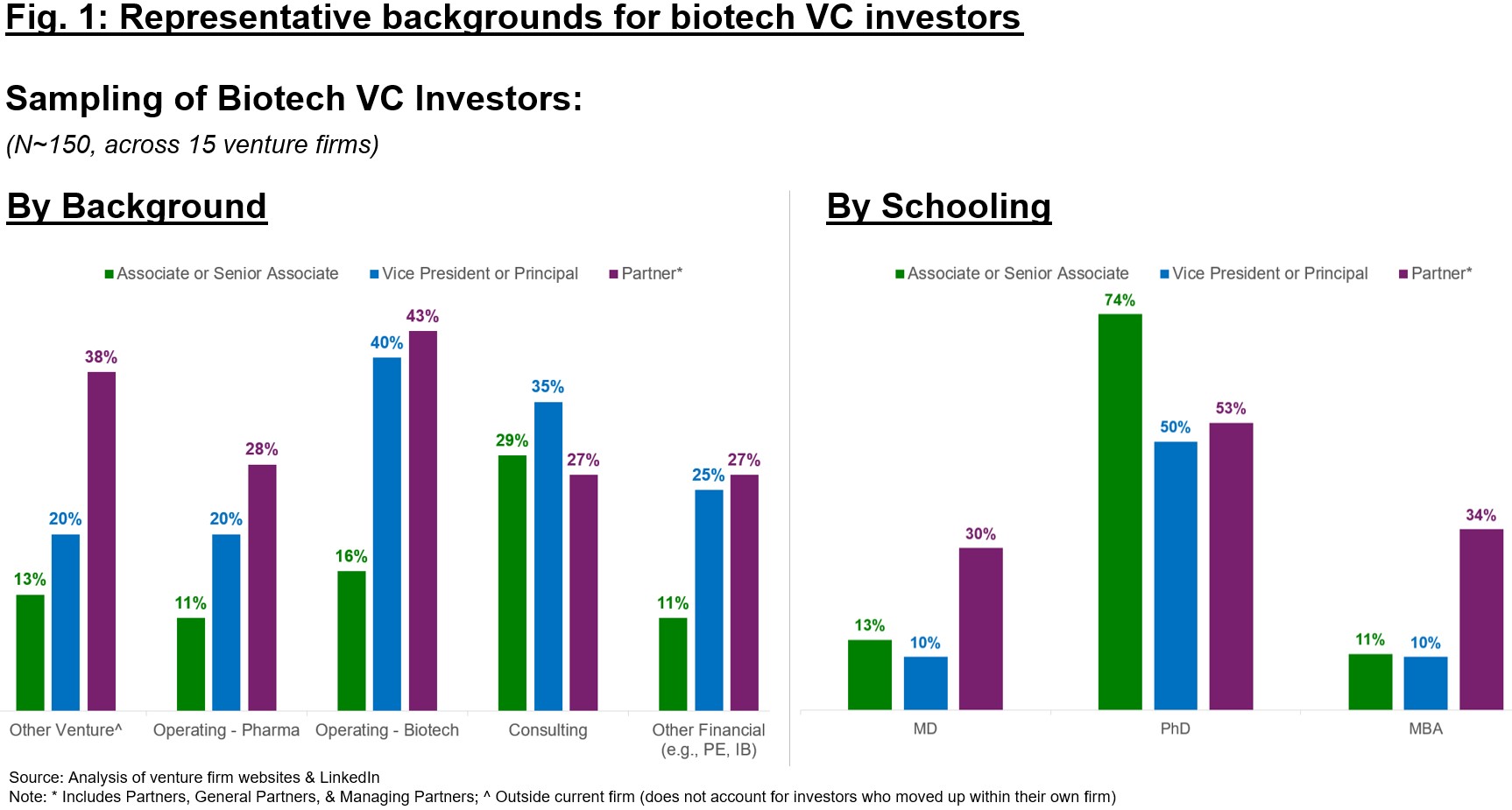

Who’re the buyers that make up these VC companies? Biotech enterprise capitalists can come from a wide range of backgrounds, although a number of classes are most typical. As an example the varied backgrounds and relative frequency, ~150 buyers throughout 15 companies had been sampled as a consultant lower of biotech VC spanning early to later-stage companies ( 1). Some notable findings from this evaluation are as follows:

-

- Many VCs, even when they begin on the Affiliate degree, have some degree of labor expertise post-schooling. On the Affiliate degree, consulting is likely one of the extra prevalent backgrounds, with ~30% of Associates having frolicked in consulting. Working expertise (whether or not in Pharma or Biotech) additionally accounts for a considerable share, 10-15% for every. ~15% of Associates could are available with prior enterprise expertise, and a smaller ~10% could have monetary backgrounds outdoors enterprise (e.g., Personal Fairness, Funding Banking). For barely extra senior roles (VP and Principal), naturally extra of those roles are crammed by candidates who’ve already frolicked in VC as Associates at different companies (~20%), or else they’ve been promoted via the ranks at their very own companies. Working expertise can be far more widespread for VPs / Principals (by ~2x), as is different monetary roles. On the accomplice degree, expertise at different VC companies is kind of widespread (~40% of the pattern), as is working expertise both in Pharma (~30%) or Biotech (~45%), whereas shares of Companions with both consulting or different monetary backgrounds are related (~30%).

- From a tutorial coaching perspective, many biotech funding workforce professionals have some kind of superior diploma, although certainly not is it a pre-requisite. PhD is the most typical educational background (50-75% of sampling, throughout seniority) adopted by MD and MBA (every 10-35%).

- VC could be a lifetime profession, and thus unsurprisingly tenures for buyers at particular person funds will be fairly lengthy. Within the aforementioned dataset, the common tenure of an investor at their present agency was >2 years for Associates / Sr. Associates, ~5 years for VPs / Principals, and almost 10 years for Companions.

Fast abstract: There are a number of entry factors into VC – on the Analyst / Affiliate / Sr. Affiliate degree (commonest), on the VP / Principal degree, or on the Associate degree. Throughout every, varied units of expertise and background are widespread.

What does a “day within the life” appear like? It’s an excellent query that’s incessantly requested, however the unsatisfying reply is that even for a person investor at a targeted agency, two days hardly ever resemble one another. VC is a dynamic and far-ranging ecosystem and thus the subjects and varieties of actions vary broadly. What’s common is the 24/7 nature of VC – excellent news and dangerous information alike don’t persist with a Mon-Fri schedule, and thus a lot of investing is analyzing data on the fly when partial datasets can be found and coming to suggestions or choices rapidly. VC can come throughout as a glamorous life-style of networking, however whereas making connections is definitely one facet of the function, it’s dwarfed by a lot of the onerous work that goes into the day-to-day actions.

Extra “typical” actions will be damaged into 3 classes (1) energetic diligence for brand spanking new offers within the pipeline, (2) firm constructing (if relevant – see above on early-stage VC nuances), and (3) portfolio & fund administration.

- Diligence: Throughout companies and no matter stage, diligence will typically be a key focus for buyers. An investor is launched to a brand new firm or perhaps a idea (if an organization has not but been fashioned) and, typically in collaboration with different workforce members, advisors, KOLs, and many others. should decide on whether or not or to not put money into the corporate or thought. I wrote a separate piece on exemplary diligence subjects (right here), which outlines among the subjects one may concentrate on in an preliminary diligence.

- Firm Constructing: Concepts for brand spanking new corporations can come from entrepreneurs, academia, or emerge from in-house ideation on a brand new know-how or product thesis. Whatever the supply for the newco, oftentimes early-stage VC outlets play a job in turning an thought right into a product and firm. Whereas completely different companies have completely different types, newco creation typically entails the “customary” diligence on science or asset(s), but in addition encompasses workforce constructing, drug discovery funnel institution (incl. assay set-up or improvement), asset in-licensing, scientific trial design, partnering (with CRO/CDMOs, different biotech, TTOs, and many others.), strategic components (e.g., pipeline or indication prioritization), budgeting, institution of a near- and long-term plan to realize key milestones, and pitching to different buyers. Not each VC agency will pursue firm creation, however for those who do it’s a nice alternative for buyers to roll up their sleeves and serve in interim or part-time working roles to assist new corporations obtain the following inflection.

- Portfolio & Fund Administration: Energetic portfolio firm administration is a big a part of the function, particularly for extra senior buyers. Oftentimes an investor function comes with some kind of illustration on a Board of Administrators, whether or not as a Director or Observer, and the chance to share views with firm administration. A VC agency may also carefully monitor its portfolio in order that its buyers (LPs, or Restricted Companions) keep updated on portfolio developments. Fundraising is a key exercise (particularly for Companions) and powerful relationships with LPs are important for any sustainable VC agency.

Fast abstract: Whereas no two days are the identical, the flexibility to independently and collaboratively diligence a brand new firm or thought is essential to the VC skillset. Relying on the kind of agency, firm constructing and portfolio & fund administration might also kind a big a part of a person investor’s mandate.

How does one break into VC? Many extra candidates need to break into VC than there are roles accessible, so it’s vital to think about the quantity of potential openings and logistic elements like location when assessing the percentages of touchdown a proposal. That is all extremely illustrative, however should you assume the ~90 or so U.S. VCs with AUM >$1B (a very good proxy for a fairly sustainable agency that can possible rent sooner or later), you may estimate that roles sometimes open (1) when somebody on the agency leaves or (2) when the agency raises a brand new fund and / or will increase the variety of buyers on the workforce. Assuming (once more, very “directionally,”) a brand new fund is raised each 2-5 years and there’s some pure turnover particularly within the extra junior roles, one may estimate that 30-70 Affiliate (or related) roles turn into accessible yearly for biotech VC companies. Many of those roles might be targeted in “hubs” (Boston, SF / Bay Space, and more and more NY) and will be fairly aggressive. Beneath are sources and suggestions for these contemplating a job in VC.

-

- To search out out about new roles, it’s vital to remain on prime of any publicized job postings in addition to construct your community in order that you’ll hear via the grapevine when a agency is recruiting. Typically companies will submit on their web site or LinkedIn for brand spanking new roles, however extra typically they depend on word-of-mouth suggestions and / or a recruiting agency to assist supply expertise. If you’re trying to keep on prime of potential job openings, I like to recommend following prioritized companies on social media in addition to constructing your community via occasions, informational interviews, and many others. to remain on prime of openings as they arrive up.

- Given the above numbers, you’ll possible need to be sure to are comfy in your present place to present the VC job search 3-9 months, given roles turn into accessible considerably sporadically and are sometimes tied to a agency’s fundraising. Be ready to attend for the best function to come back up.

- Each agency is exclusive in its personal manner – breadth of funding focus, degree of technical diligence, working norms, tradition, and many others. Do your diligence earlier than kicking off the method to determine companies that on paper match most along with your background, profession aspirations, pursuits, and logistical issues. Then, whereas interviewing, be sure to are asking inquiries to assess match and gathering enter from trusted advisors or mentors on varied companies. You solely have one shot to make an excellent first impression, so set your self up for achievement in your first enterprise function by doing all of your homework and assessing whether or not every agency is actually a spot you’ll each add and achieve worth.

- Associated to the above, take into consideration a ability or perspective you might have that makes you distinctive not directly. Oftentimes buyers are searching for colleagues to (politely and judiciously) problem opinions or search for the contrarian thesis. This differentiation can take time to construct, so don’t really feel like it’s essential rush into VC proper out of academia – the trade is small, so that you need your first function in VC to make a powerful impression.

- Lastly – if you’re fortunate to just accept a job in VC, put together your self for a steep studying curve! VC may be very a lot an apprenticeship mannequin, so there might be quite a bit you’ll be able to’t put together for forward of time. An open thoughts, gregarious perspective, and humility will carry you far.

On the finish of the day, whereas the trade could appear opaque, you will see that that it’s comprised of extremely motivated people who’re (at instances doggedly) obsessed with bettering the well being prospects for sufferers in want. The chances of a product or an organization being profitable are very slim given terribly low success charges of drug discovery and improvement – it takes numerous humility, dedication, ardour, and empathy to achieve this enterprise. I hope this submit has supplied a glimpse into the fast-paced and team-oriented nature of early-stage biotech VC, and good luck to any potential candidates!